5 minute read

Editor's note: This article was updated on June 5, 2023 from its original publish date of January 16, 2020.

Digital wallets are officially mainstream. Digital wallet usage will exceed 4.4 billion globally by 2025. Here we explain how digital wallets work, their benefits and ease of use, and what everyone from small business owners to global brands can do to accept them.

Digital wallet usage will exceed 4.4 billion globally by 2025.

What is a digital wallet?

A digital wallet is a virtual wallet that stores a user's various payment types on an app or browser. They can be used on a laptop, tablet, smartphone, smartwatch or other wearables. Popular digital wallets include Google Pay, Alipay, WeChat Pay and Apple Pay. While the ability to tap and pay with a digital wallet looks easy, several technologies operate behind the scenes to enable them. The good news? These technologies require no extra effort to deploy and enable.

So how does it work? Here's a quick rundown.

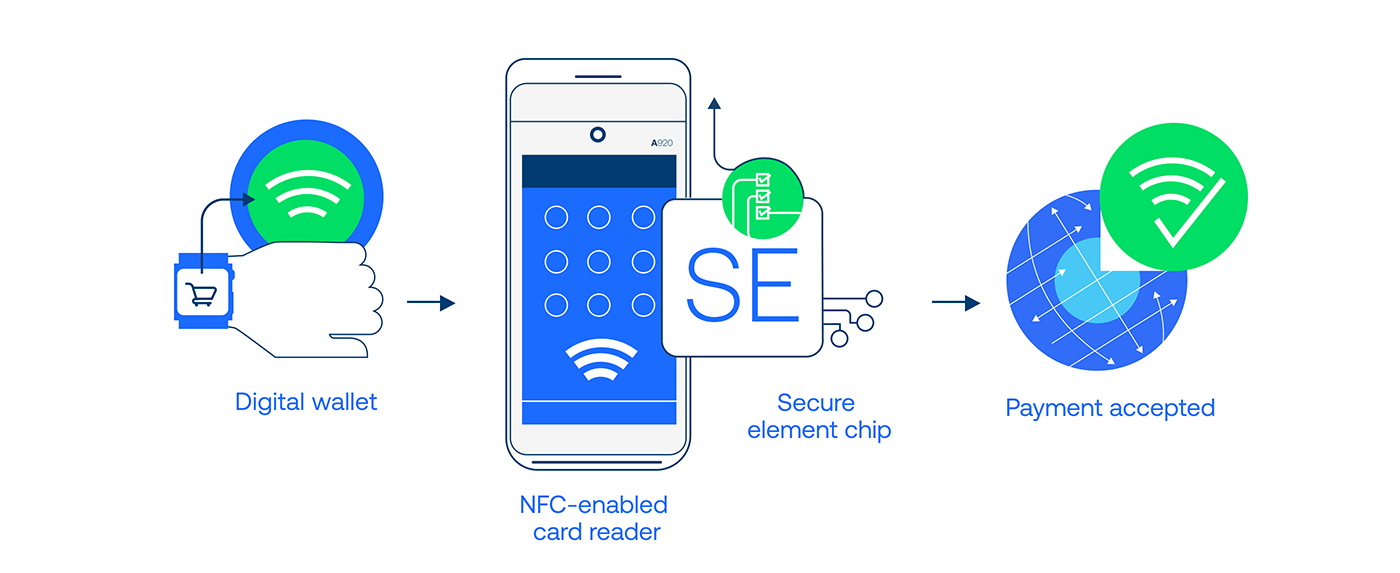

Near-field communication

Near-field communication (NFC) technology allows two devices to communicate. In-store shoppers simply wave or tap their mobile device over a card reader to make a contactless payment. Then their smartphone transmits financial data to the NFC-enabled card reader when they checkout.

Encryption

Many software programs use encryption to keep data safe. Information is encrypted and can only be decoded by a user with the correct encryption key—or token. Encrypted data will appear scrambled to a user attempting to access the data without permission. This technology—while not exclusive to digital wallets—keeps consumers' personal and financial information safe and secure.

Tokenization

Used in conjunction with data encryption, tokenization secures the end-to-end payment process, ensuring a consumer's financial information is never exposed. Personal data—including credit card number, expiration date and checking account information—is disguised with a single-use token that acts as a stand-in data set to complete the transaction. That means a consumer's information is safe in the future from fraudsters since the code expires after one use.

Payment rails

Digital wallets take advantage of the traditional payment infrastructure—or payment rails—that already exists. That means digital wallets rely on the same, reliable networks and processors, allowing you to sell more, faster.

Why you should accept digital wallets

Whatever your size, scale or industry, accepting digital wallets carries many benefits. Advantages include:

- A seamless customer experience with minimal friction. Digital wallets are easy to use—and access—from any device. And they make paying fast.

- Enhanced security. Digital wallets rely on tokenization. It hides sensitive customer information.

- Better authorization rates. Digital wallets use tokenization, which increases authorization rates.

- Faster online checkouts. When customers pay with their digital wallets, they pay directly with a fingerprint or face scan in real time. This means they don't have to pull out a card to pay in store or manually enter their credit card information online.

Upgrade your point of sale—online and in person

As more consumers adopt digital wallets as their go-to payment method, make sure your point of sale is NFC-enabled for contactless payments. And be sure to include popular digital wallets in your online offerings.

For brick-and-mortar businesses, customers can open their digital wallet from their mobile device, select their stored card of choice, then tap their device near the card reader to complete their transaction. No physical card, wallet or purse is required.

You can also simplify your online checkout process by accepting digital wallets. Customers simply choose a stored card in their digital wallet and then click to buy. They enable their wallet to authorize their payment with a passcode, face recognition or finger scan.

Digital wallet users are growing. Are you ready?

Need more reasons to upgrade? A recent study by Visa indicates that 48% of consumers won't even shop at stores that don't offer contactless payment options.

The numbers are clear—consumers are embracing digital wallets like never before, both online and in store, and you need to be prepared. We make it easy for you to accept digital wallets. Our developer tools and cloud-based POS solutions enable secure and easy-to-use payment services. And our customer support teams can help with any questions you have along the way. Contact us today to get started.